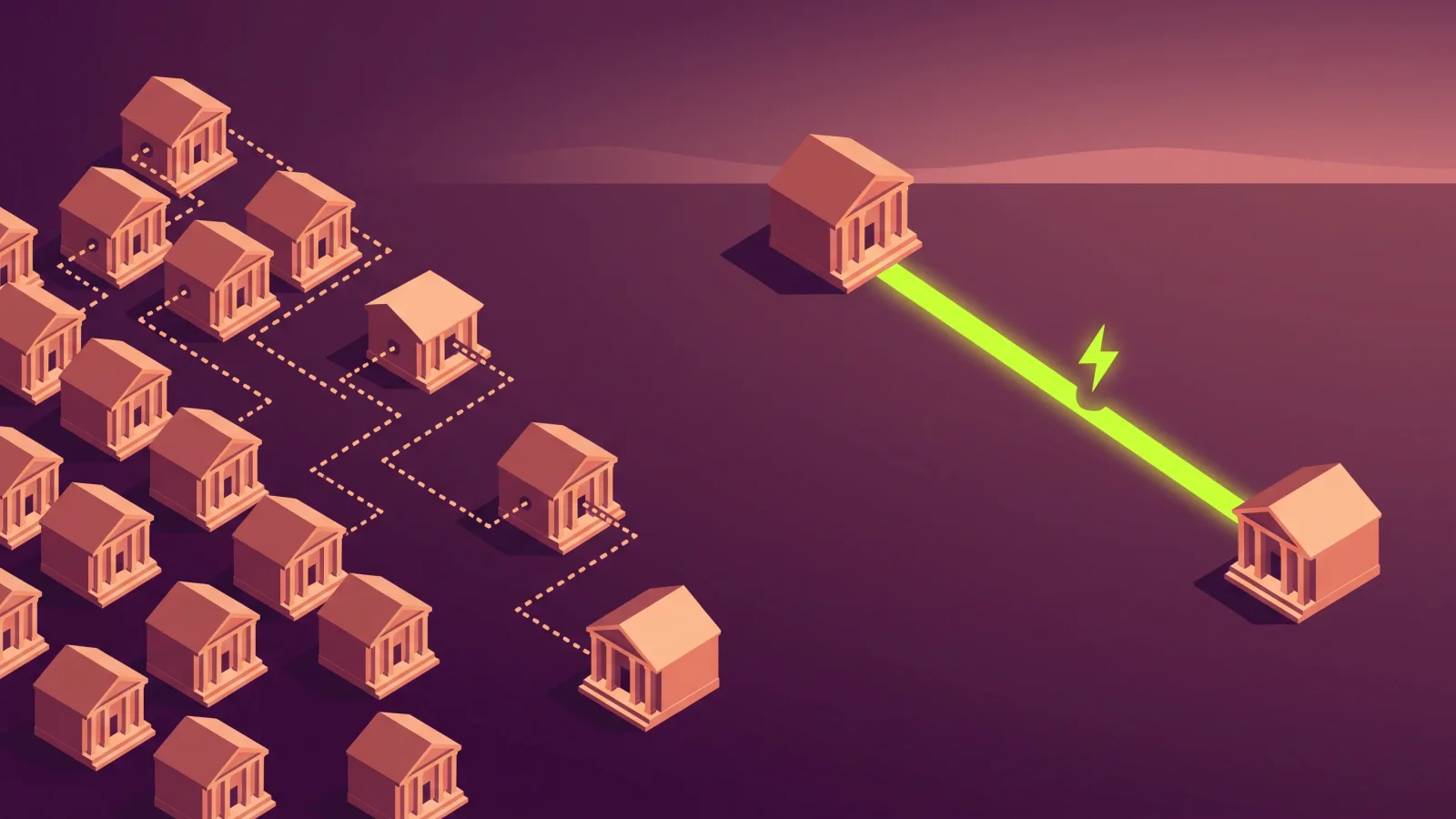

Cross-border payments without correspondent banking route value directly between sender and receiver instead of hopping through a chain of intermediary banks. Networks like Lightning, Bitcoin's payment layer, can act as a neutral FX layer: they carry value in bitcoin, convert to the currency each side wants at the edges, and settle in under a second instead of days.

What does cross-border payments without correspondent banking mean?

It means settling a payment between two countries without routing it through the network of intermediary banks that normally connect one bank to another. In the traditional model, a bank without a direct presence in the destination country relies on correspondent banks that hold accounts for each other. Removing that chain lets the two ends settle directly.

Correspondent banking is the system banks use to move money across borders. A bank in one country funds an account (a nostro account) at a partner bank abroad, and a payment hops from institution to institution until it reaches the destination. Each hop adds a fee, an FX spread, and a delay. A 2026 Federal Reserve research note on payment stablecoins and cross-border payments states the problem plainly:

"Cross-border payments are generally viewed as slower, more expensive, and not very transparent to end-users relative to domestic payments."

How does correspondent banking compare to a Lightning FX layer?

The two models differ on almost every axis a business cares about: how long settlement takes, how many parties touch the money, how much capital sits idle to make it work, and what happens outside banking hours. A Lightning FX layer removes the intermediary chain and settles directly, which changes the cost and speed profile at the same time.

| Dimension | Correspondent banking | Lightning FX layer |

|---|---|---|

| Settlement time | 1 to 5 business days | Under one second |

| Intermediaries | Several banks in a chain | None between the two ends |

| Operating hours | Business days, banking hours | 24/7, including weekends |

| Pre-funded capital | Nostro and vostro accounts held abroad | No pre-funded foreign accounts |

| Currency conversion | FX spread applied at each hop | Converted once at the edges |

| Cost visibility | Fees deducted along the way | Fee known before sending |

The point of the table is not that one column is always right. Banks still clear enormous value through correspondent networks. The point is that for a business moving money across borders, most of the cost and delay lives in the intermediary chain, and that chain is exactly what a direct settlement layer removes.

Why is correspondent banking slow and expensive?

Because every hop adds time, cost, and a point of failure. A single payment often passes through several banks, each taking a fee and an FX spread on its own schedule. The same Federal Reserve note reports that over 60 percent of wholesale payments are routed through one or more intermediaries, and a payment "needs to be processed by each intermediary in the chain" before it lands.

The network carrying those payments has also been shrinking. The number of active correspondents has declined by about 30 percent over the last decade, according to the Federal Reserve's analysis of correspondent banking trends. Fewer correspondents means longer chains on the routes that remain, which raises cost per payment on exactly the corridors that already carried the most friction. Every fee in that chain is charged on top of the amount you actually send.

How does the Lightning Network work as a neutral FX layer?

Lightning uses bitcoin as a bridge asset. A payment enters as one currency, moves across the network as bitcoin, and converts to the currency the recipient wants at the far edge. Neither side has to hold the same asset, and no bank in the middle holds the funds. The conversion happens once, at the point of entry and exit, rather than at every hop.

Lightning (Bitcoin's payment layer that settles transactions in under a second for fractions of a cent) records balances in payment channels, a two-party balance held open between two wallets. Bitcoin is the routing backbone, and other currencies are expressed in terms of it. Dollar-pegged stablecoins ride the same rails: Taproot Assets route over the existing Lightning Network with no node upgrade or opt-in, so a business can accept a stablecoin and settle in bitcoin, or the reverse, on one integration.

The volume behind this is not theoretical. USDT on-chain volume topped $10 trillion in 2024, closing in on the annual throughput of major card networks. Live network capacity, node count, and channel count are tracked on the Amboss Lightning network explorer. The same design that removes intermediaries also removes the idle capital banks keep abroad. Circle, issuer of the USDC and EURC stablecoins, describes the shift directly:

"Stablecoin-based payment flows may reduce the need for pre-funded nostro accounts by enabling direct settlement at the time of payment."

What does moving money cross-border on Lightning cost?

Far less than the stacked fees of a cross-border card or wire. On cards, an international payment that also needs currency conversion pays the base rate plus two surcharges. Stripe's published pricing is 2.9% + 30¢ per transaction, plus 1.5% for international cards and another 1% when currency conversion is required, which stacks to 5.4% + 30¢ on a converted cross-border charge.

On Lightning, the routing fee is a fraction of a cent regardless of the amount or the destination, because the network charges for moving value, not for crossing a border. Stablecoin transfers land in the same range: Circle notes that on-chain stablecoin fees are "typically measured in cents (or less) per transaction." The FX conversion still has a cost at the edges, set by whoever provides local liquidity, but the correspondent chain and its per-hop spreads are gone.

What are the trade-offs of skipping correspondent banking?

The model is not a drop-in replacement for every corridor, and it is worth being honest about where it stops. A Lightning FX layer moves value between two points fast and cheap, but the currency conversion at each edge still depends on someone providing local liquidity, and that price varies by market. Thin corridors can cost more to convert than deep ones.

There are three other constraints to weigh:

- On and off ramps. If you need funds in a domestic bank account, you still convert to local fiat through a partner. The rail removes the intermediary chain, not the final banking step.

- Bridge-asset exposure. Value transits as bitcoin. For payments that settle in under a second the exposure window is tiny, but treasury and accounting still have to account for it.

- Wallet and counterparty coverage. Both ends need software that speaks the rail. Coverage is expanding quickly across wallets and processors, but it is not yet universal in every region.

For businesses whose cost and delay live in the correspondent chain, those trade-offs are usually smaller than the fees they replace. For a business whose only need is a domestic card charge, the old rails may still be simpler.

Where does Amboss Payments fit?

Amboss Payments is the part of this a business actually integrates. It accepts bitcoin and stablecoin payments over Lightning on one integration, so a customer can pay in one currency while you settle in the form you want, without running foreign bank accounts or picking a chain. It handles the payment rail and the conversion at the edges. It does not replace your bank, your accountant, or your local off-ramp, so if you need funds in a domestic account you still arrange that step yourself. If cross-border cost and settlement delay are the problem you are solving, Amboss Payments is where to start.

Frequently asked questions

Can you send cross-border payments without a correspondent bank?

Yes. A direct settlement network like Lightning routes value between sender and receiver without the intermediary banks that correspondent banking relies on. Value moves as bitcoin and converts to the currency each side wants at the edges. The correspondent chain, its per-hop fees, and its FX spreads are removed, though you still convert to local fiat if you need funds in a domestic bank account.

How fast are Lightning cross-border payments?

A Lightning payment settles in under a second, at any hour, including weekends and holidays. Correspondent-banking payments typically take 1 to 5 business days because each intermediary in the chain processes on its own schedule. The speed difference comes from removing the intermediaries entirely: with no chain to traverse, the payment reaches the recipient the moment it is sent.

Does using a Lightning FX layer mean holding bitcoin?

Not as a treasury position. Bitcoin is the bridge asset the network uses to move value, but a business can accept a stablecoin and settle in the form it wants, with the conversion handled at the edges. You interact with the currencies you choose. Whether you keep any bitcoin balance is a separate treasury decision, not a requirement of using the rail.

What currencies can move over a Lightning FX layer?

Bitcoin is the only thing that actually moves across the network. It is the value carried between the two ends on every payment. Dollar-pegged stablecoins like USDT and USDC, and euro-pegged ones like EURC, live only at the edges: the sender converts into bitcoin to send, and the recipient converts out into the currency they want. The core rail is always bitcoin, so the two sides never have to hold the same asset.

Is a Lightning FX layer cheaper than a wire or card for cross-border payments?

Usually, yes. A cross-border card charge that needs conversion can reach 5.4% plus a fixed fee once international and FX surcharges stack, and wires carry per-hop spreads through the correspondent chain. Lightning routing fees are a fraction of a cent regardless of destination. The remaining cost is the currency conversion at the edges, priced by local liquidity, which is where most of the real cost now sits.